All Categories

Featured

2 individuals purchase joint annuities, which give a guaranteed revenue stream for the remainder of their lives. If an annuitant passes away throughout the distribution period, the staying funds in the annuity may be passed on to a designated recipient. The particular choices and tax obligation implications will certainly depend upon the annuity agreement terms and relevant legislations. When an annuitant passes away, the interest earned on the annuity is handled in a different way relying on the sort of annuity. In a lot of cases, with a fixed-period or joint-survivor annuity, the passion remains to be paid to the surviving recipients. A survivor benefit is a feature that makes sure a payment to the annuitant's beneficiary if they die before the annuity payments are tired. Nonetheless, the schedule and regards to the death benefit may vary depending upon the particular annuity agreement. A sort of annuity that stops all repayments upon the annuitant's fatality is a life-only annuity. Recognizing the terms and problems of the survivor benefit prior to spending in a variable annuity. Annuities go through tax obligations upon the annuitant's fatality. The tax obligation therapy depends upon whether the annuity is held in a qualified or non-qualified account. The funds are subject to income tax in a certified account, such as a 401(k )or IRA. Inheritance of a nonqualified annuity commonly causes tax only on the gains, not the whole amount.

If an annuity's assigned recipient passes away, the result depends on the specific terms of the annuity contract. If no such beneficiaries are marked or if they, too

have passed away, the annuity's benefits typically revert to go back annuity owner's proprietor. If a beneficiary is not named for annuity benefits, the annuity proceeds typically go to the annuitant's estate. Multi-year guaranteed annuities.

Annuity Rates death benefit tax

This can provide higher control over just how the annuity advantages are distributed and can be part of an estate planning strategy to handle and safeguard possessions. Shawn Plummer, CRPC Retired Life Planner and Insurance Policy Representative Shawn Plummer is a qualified Retirement Coordinator (CRPC), insurance policy agent, and annuity broker with over 15 years of firsthand experience in annuities and insurance coverage. Shawn is the owner of The Annuity Expert, an independent on the internet insurance policy

agency servicing consumers across the United States. Via this platform, he and his group aim to get rid of the guesswork in retirement planning by assisting individuals discover the most effective insurance policy protection at one of the most competitive prices. Scroll to Top. I understand every one of that. What I don't recognize is exactly how in the past getting in the 1099-R I was revealing a refund. After entering it, I now owe taxes. It's a$10,070 distinction between the reimbursement I was anticipating and the tax obligations I currently owe. That seems very extreme. At the majority of, I would have anticipated the refund to minimize- not entirely go away. An economic expert can help you determine exactly how ideal to manage an acquired annuity. What takes place to an annuity after the annuity owner dies depends upon the terms of the annuity agreement. Some annuities just quit dispersing earnings payments when the proprietor passes away. In many situations, nevertheless, the annuity has a fatality benefit. The beneficiary could receive all the remaining cash in the annuity or a guaranteed minimum payment, usually whichever is better. If your moms and dad had an annuity, their contract will certainly specify that the recipient is and may

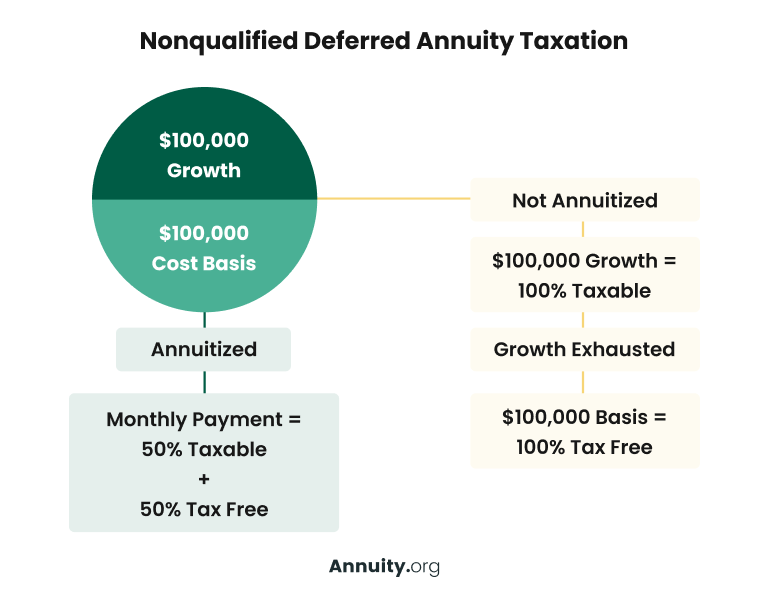

also have information regarding what payout alternatives are available for the fatality benefit. Virtually all inherited annuities undergo taxes, but exactly how an annuity is taxed relies on its kind, beneficiary standing, and repayment framework. Usually, you'll owe taxes on the difference in between the initial premium used to buy the annuity and the annuity's worth at the time the annuitant passed away. Whatever part of the annuity's principal was not already tired and any profits the annuity built up are taxable as earnings for the beneficiary. Non-qualified annuities are bought with after-tax bucks. Earnings payments from a certified annuity are dealt with as taxable income in the year they're gotten and have to adhere to needed minimum circulation rules. If you acquire a non-qualified annuity, you will just owe taxes on the incomes of the annuity, not the principal made use of to purchase it. On the other hand, a swelling amount payment can have extreme tax effects. Because you're getting the entire annuity at when, you need to pay taxes on the entire annuity in that tax obligation year. Under specific circumstances, you may be able to surrender an inherited annuity.

:max_bytes(150000):strip_icc()/Death-taxes_sketch_final-422a2456bff64e4da2f9dabb41c64ad9.png)

into a pension. An inherited IRA is an unique retirement account utilized to disperse the properties of a dead individual to their beneficiaries. The account is registered in the dead individual's name, and as a beneficiary, you are not able to make additional payments or roll the acquired IRA over to an additional account. Only qualified annuities can be rolledover right into an acquired individual retirement account.

{kind=link}

Latest Posts

Highlighting Deferred Annuity Vs Variable Annuity Everything You Need to Know About Financial Strategies Breaking Down the Basics of Variable Annuity Vs Fixed Indexed Annuity Pros and Cons of Various

Decoding How Investment Plans Work A Closer Look at How Retirement Planning Works Breaking Down the Basics of Investment Plans Pros and Cons of Various Financial Options Why Choosing the Right Financi

Breaking Down Variable Vs Fixed Annuities Key Insights on Variable Annuity Vs Fixed Indexed Annuity Defining Fixed Vs Variable Annuity Pros Cons Benefits of Fixed Vs Variable Annuity Pros And Cons Why

More

Latest Posts